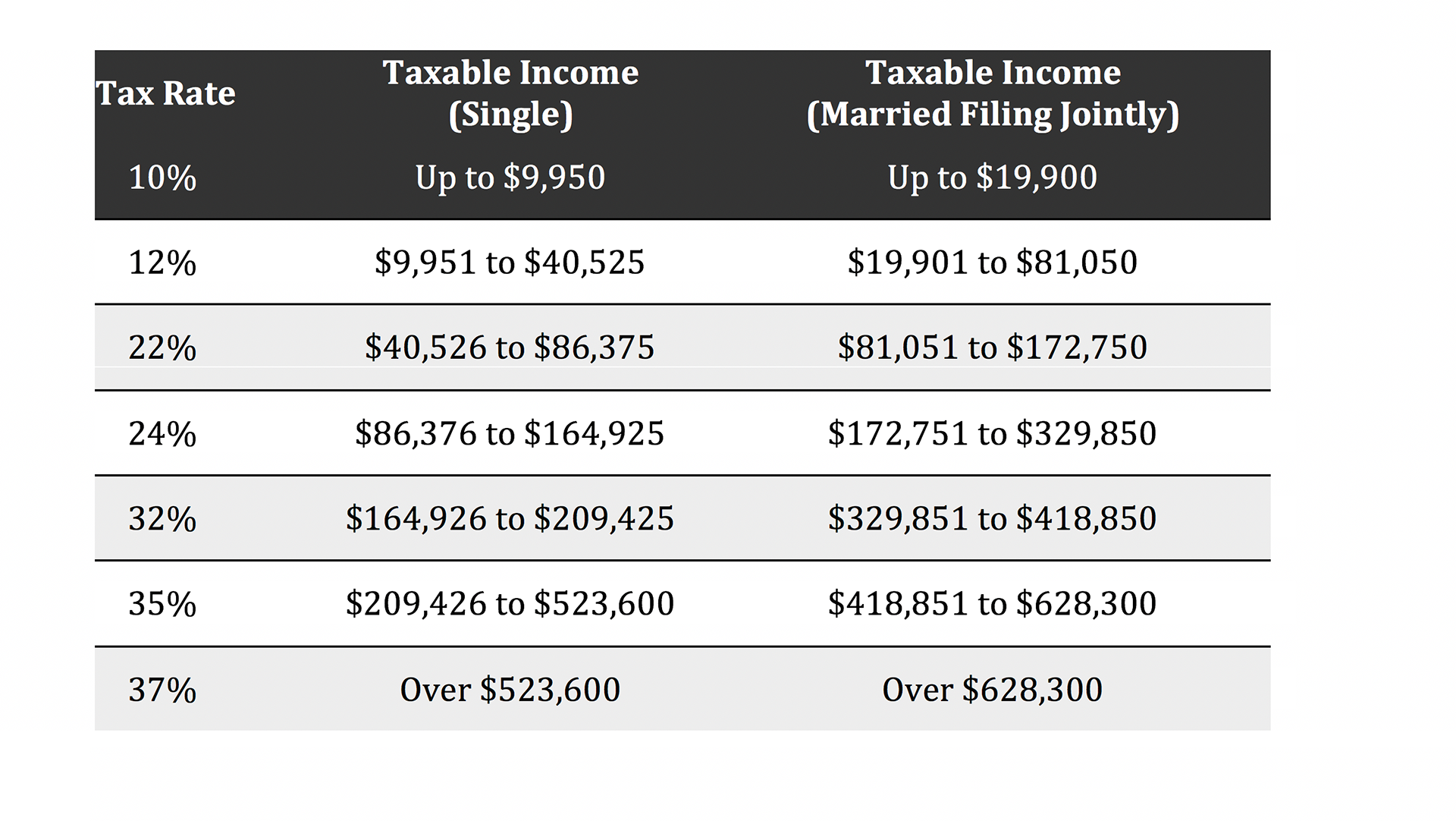

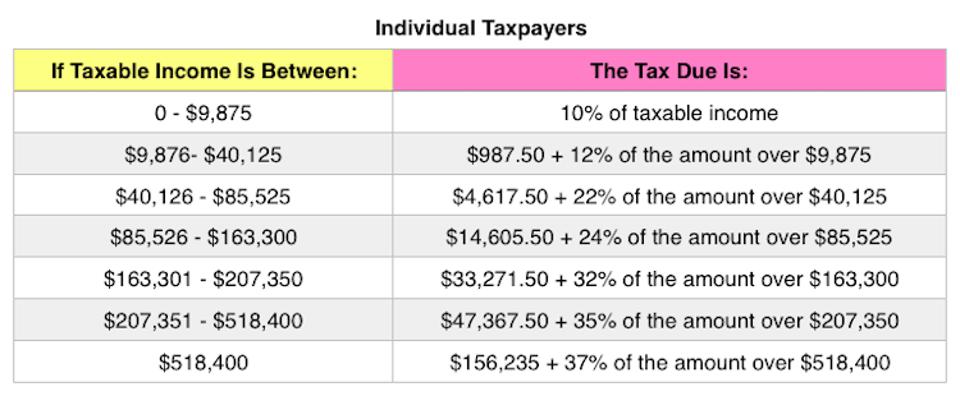

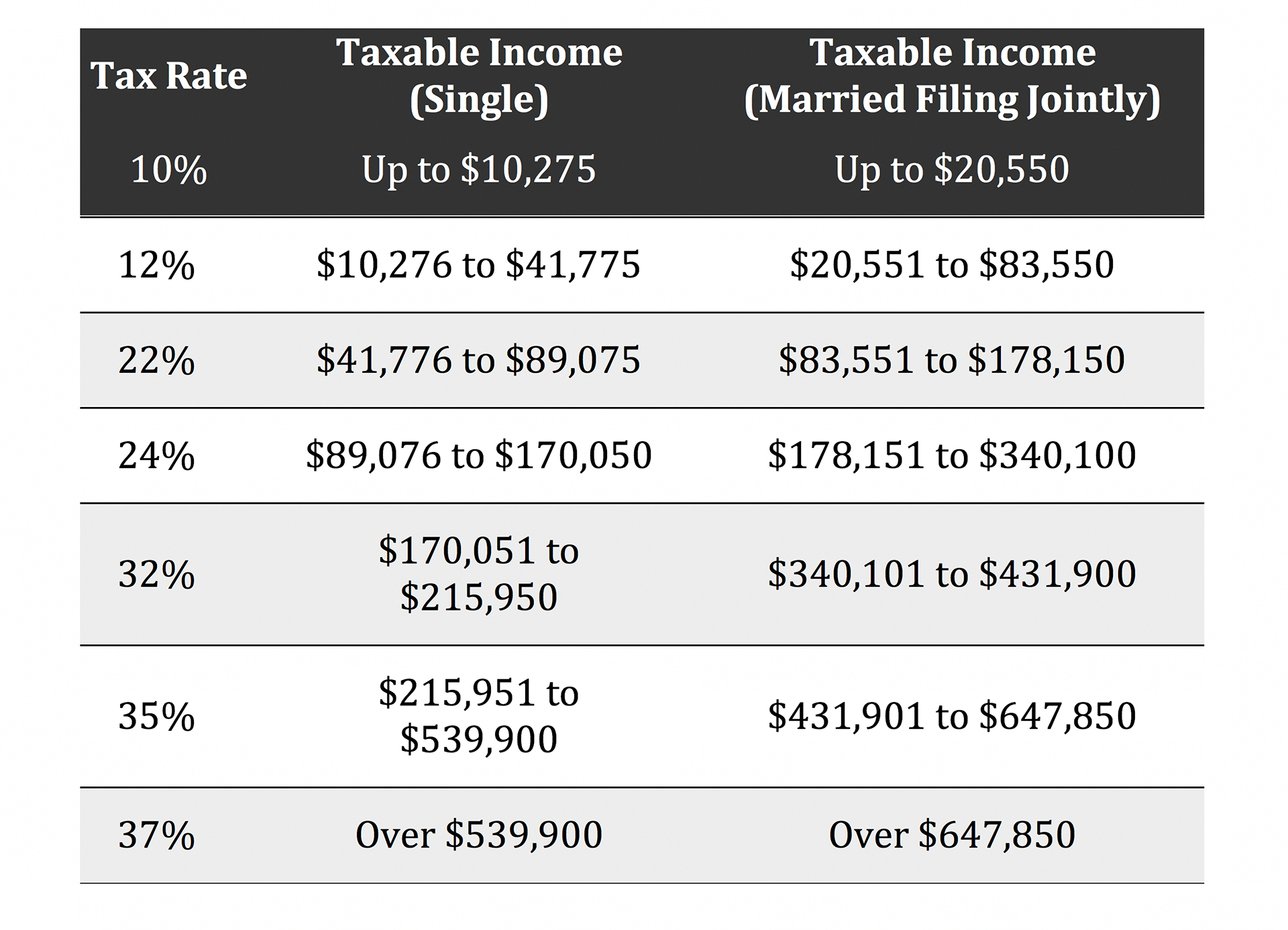

2020 Rates – Single Filers:

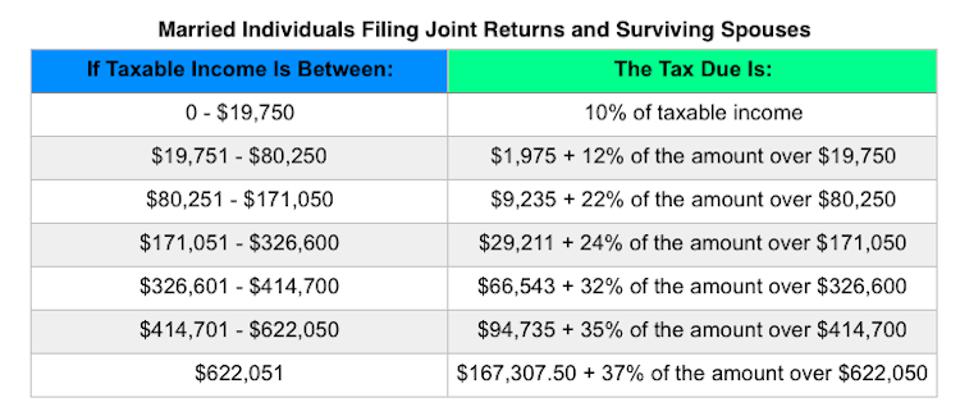

2020 Rates – Married Filing Joint:

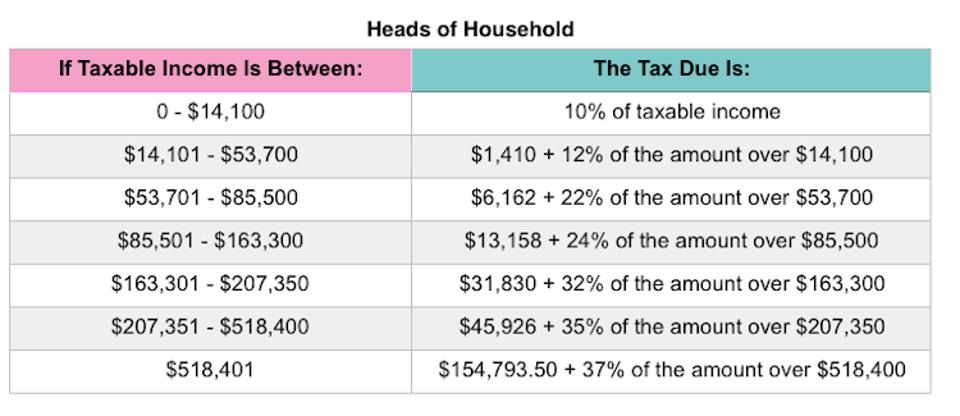

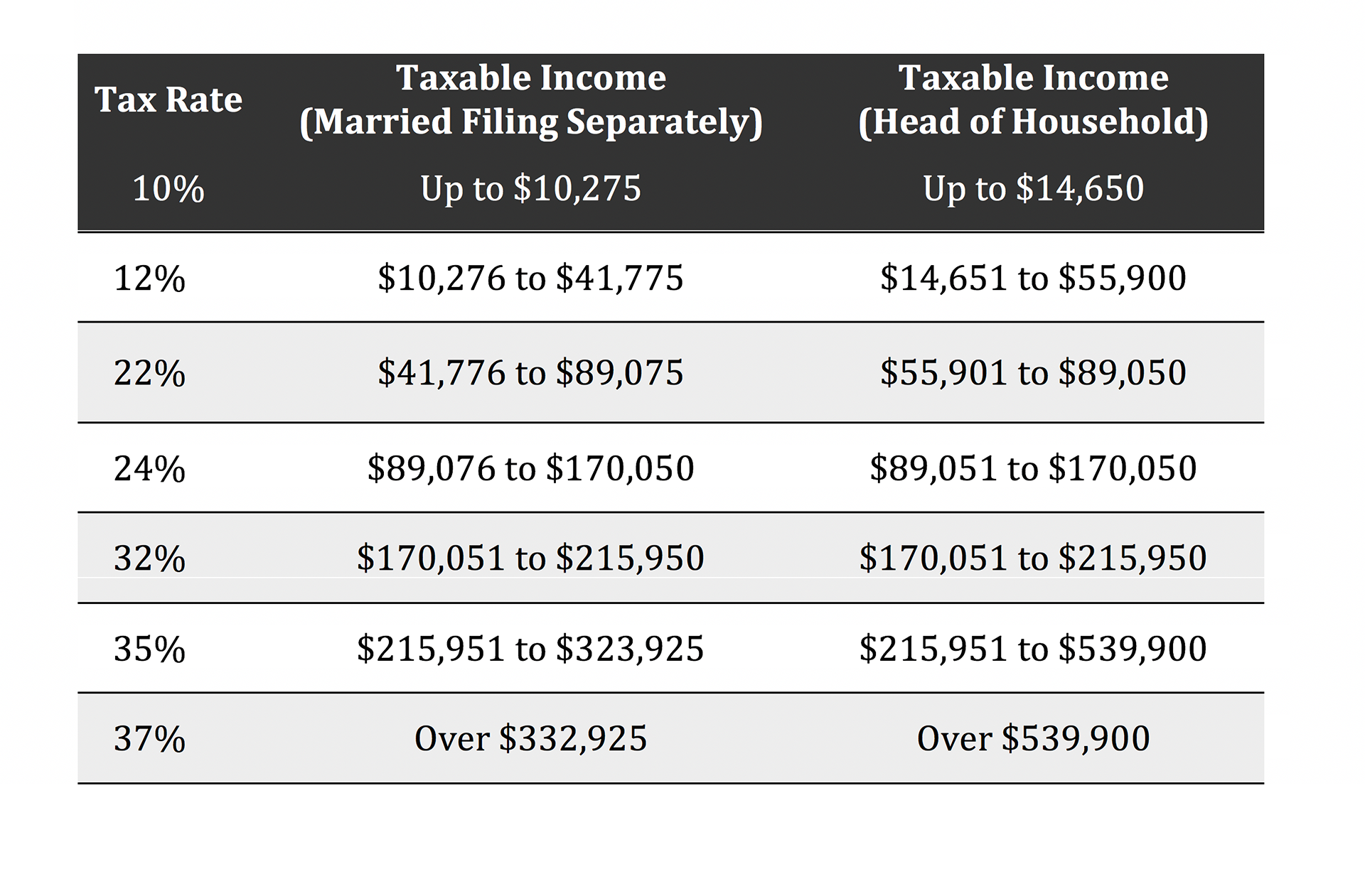

2020 Rates – Head of Household

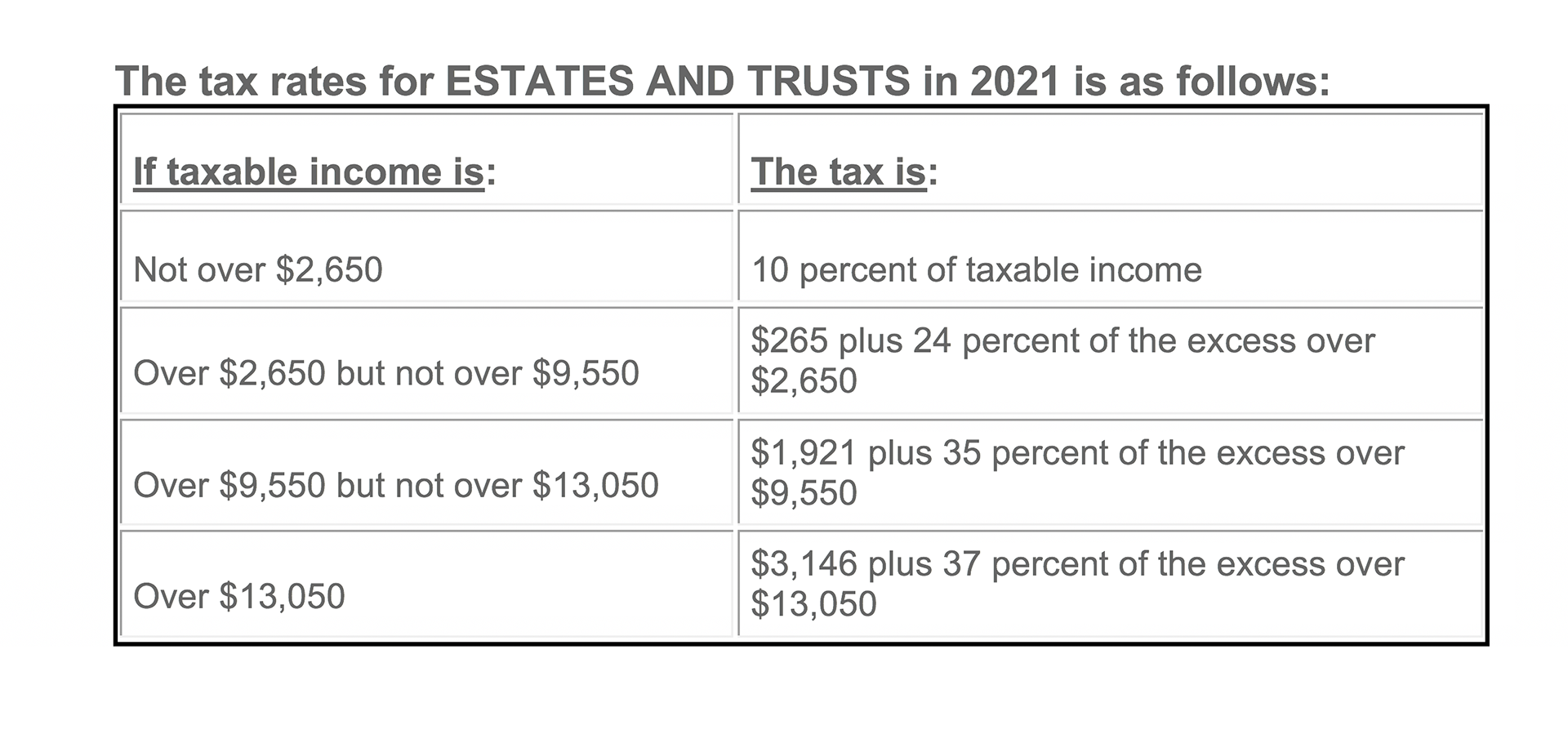

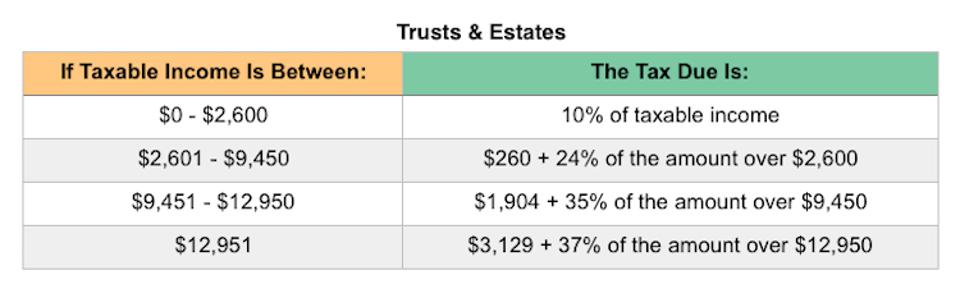

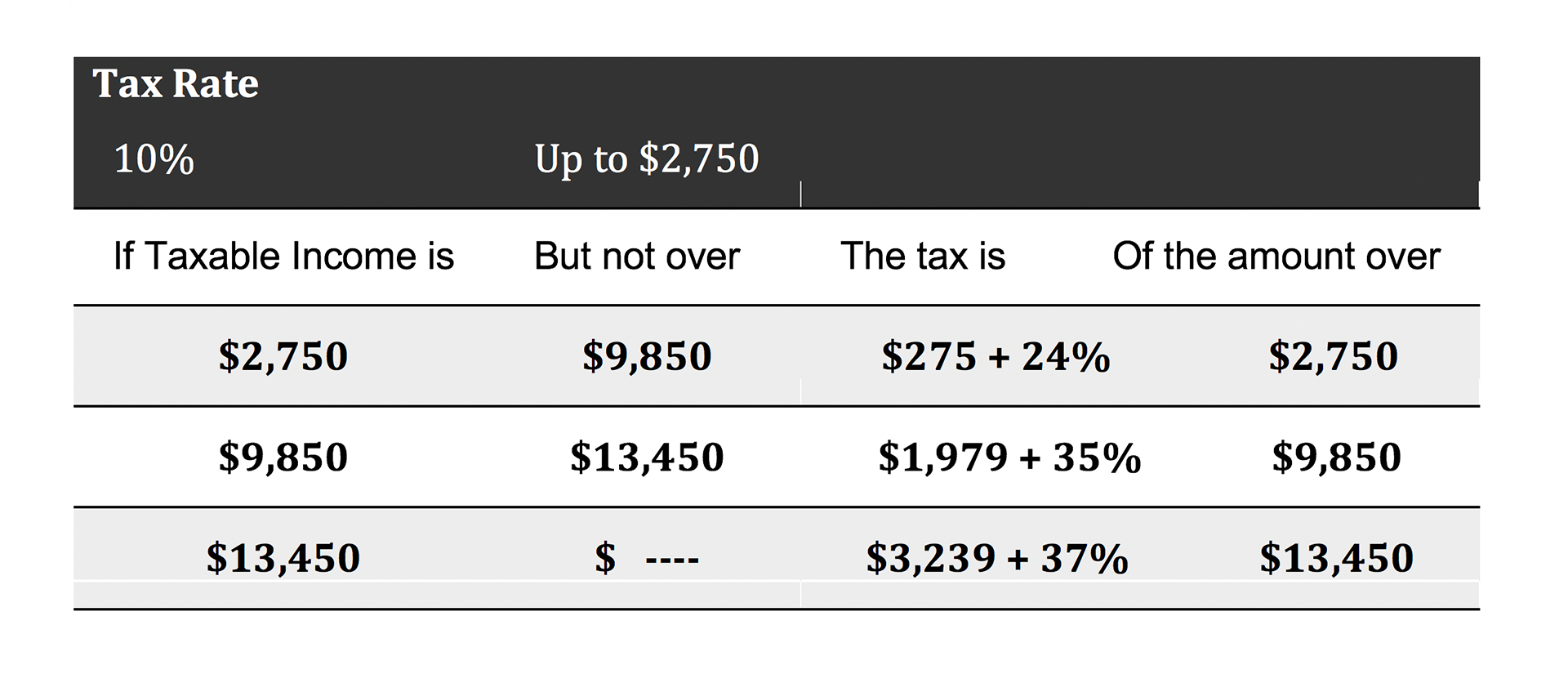

2020 Rates – Trusts & Estates:

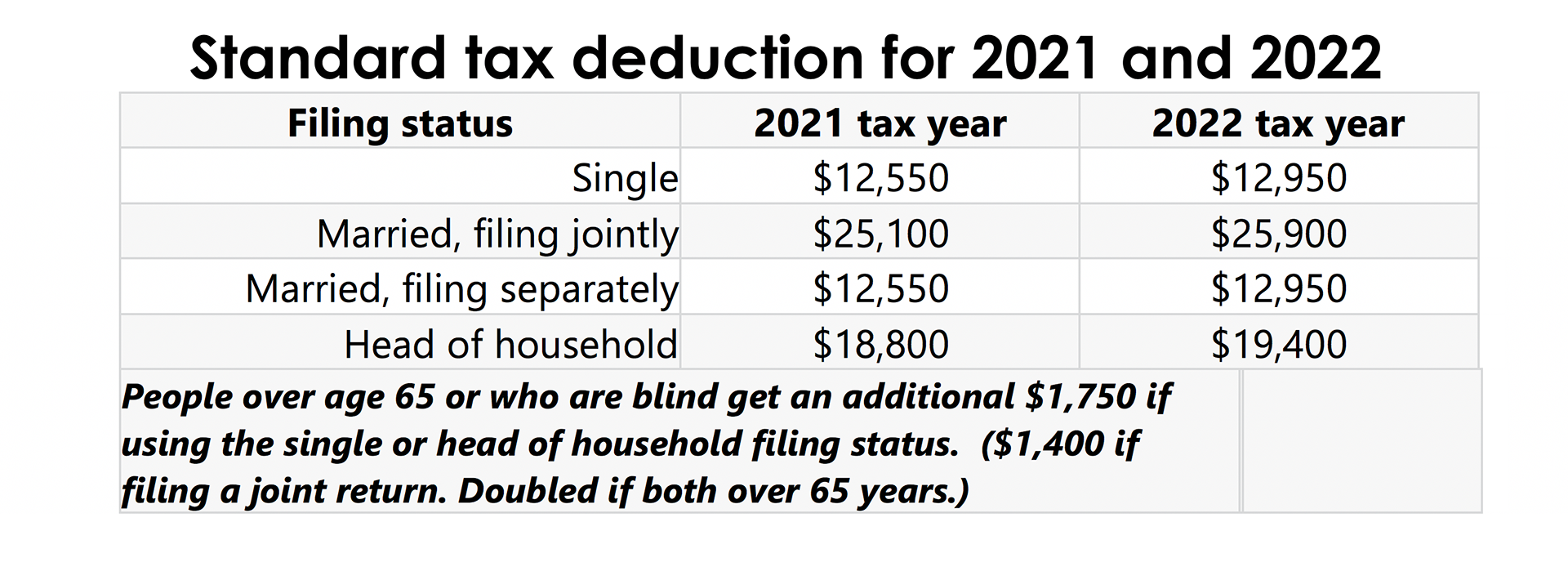

Standard Deduction Amounts 2020

Standard Deduction Amounts 2020. The standard deduction amounts will increase to $12,400 for individuals and married couples filing separately, $18,650 for heads of household, and $24,800 for married couples filing jointly and surviving spouses

For 2020, the standard deduction amount for an individual who may be claimed as a dependent by another taxpayer cannot exceed the greater of $1,100 or the sum of $350 and the individual’s earned income (not to exceed the regular standard deduction amount).

There will be no personal exemption amount for 2020. The personal exemption amount remains zero under the Tax Cuts and Jobs Act (TCJA).

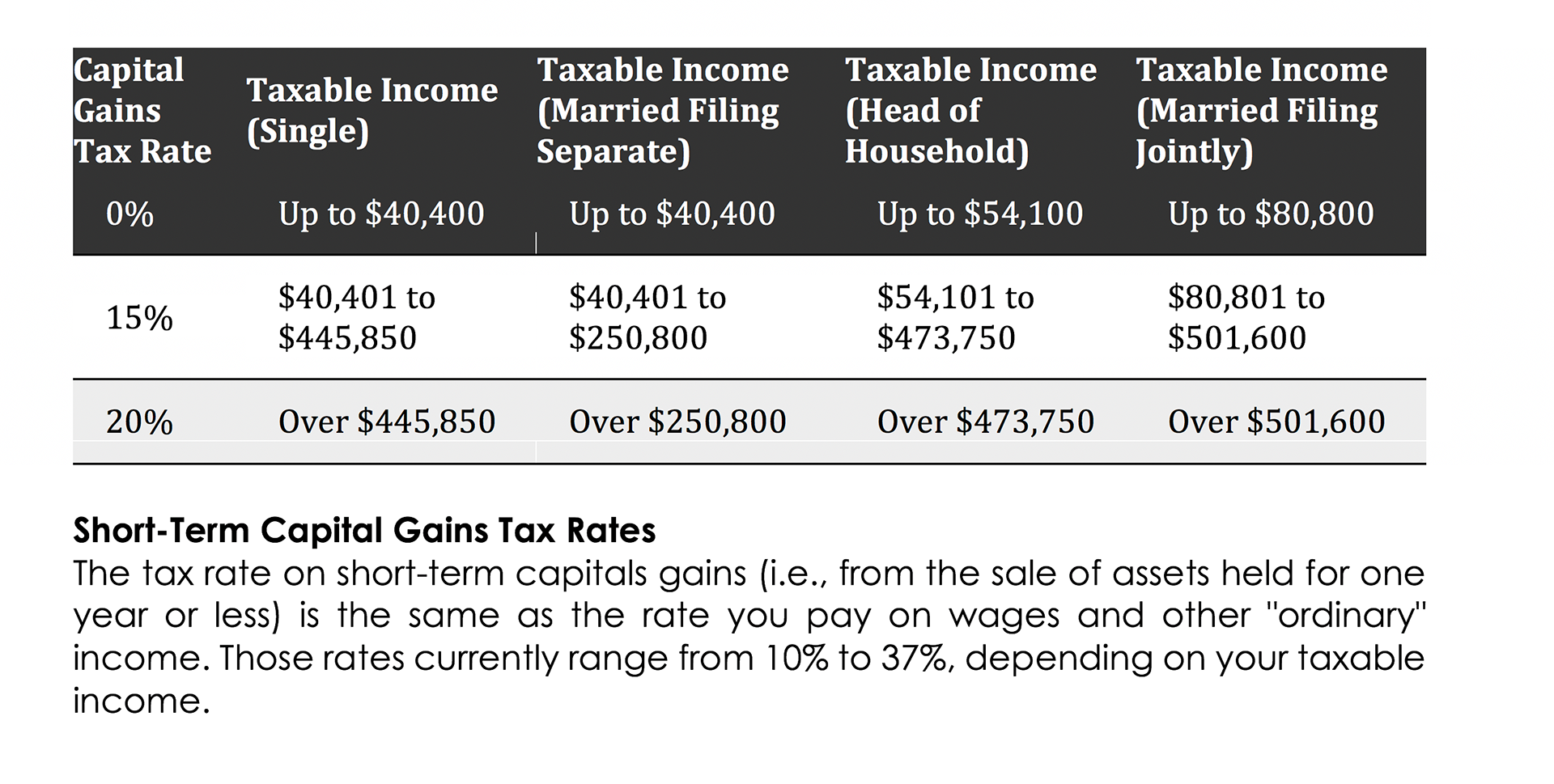

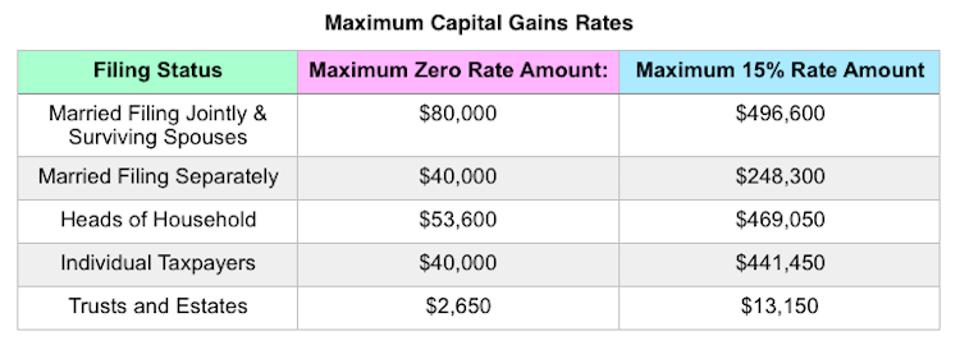

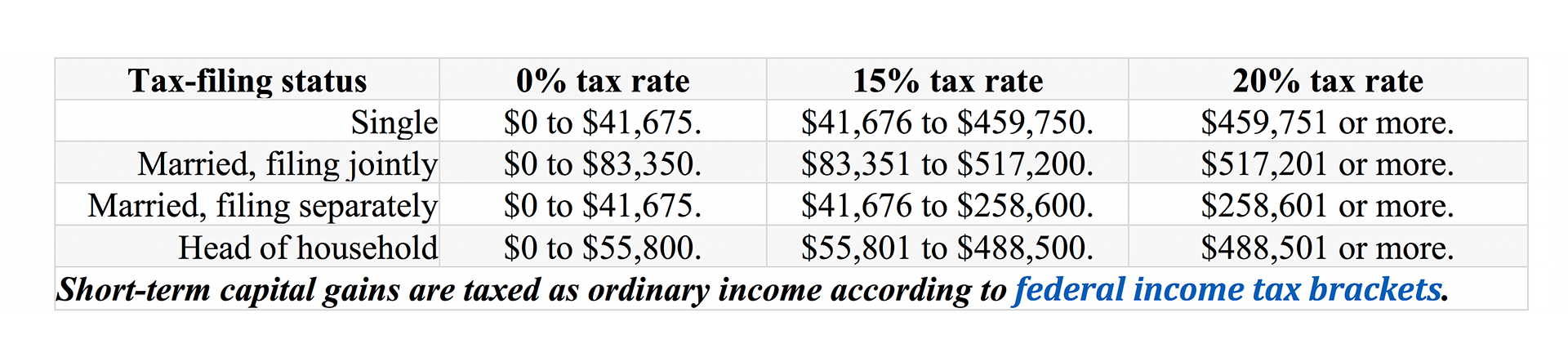

Capital Gains rates will not change for 2020, but the brackets for the rates will change. Most taxpayers pay a maximum 15% rate, but a 20% tax rate applies if your taxable income exceeds the thresholds set for the 37% ordinary tax rate. The maximum zero rate amounts and maximum 15% rate amounts break down as follows:

There are changes to itemized deductions found on

Schedule A, including:

- Medical and Dental Expenses. The “floor” for medical and dental expenses is 7.5% in 2020, which means you can only deduct those expenses which exceed 7.5% of your AGI.

- State and Local Taxes. Deductions for state and local sales, income, and property taxes remain in place and are limited to a combined total of $10,000, or $5,000 for married taxpayers filing separately.

- Home Mortgage Interest. You may only deduct interest on acquisition indebtedness—your mortgage used to buy, build, or improve your home—up to $750,000, or $375,000 for married taxpayers filing separately.

- Charitable Donations. As a result of tax reform, the percentage limit for charitable cash donations to public charities increased from 50% to 60% in 2018 and will remain at 60% for 2o20.

- Casualty and Theft Losses. The deduction for personal casualty and theft losses has been repealed except for losses attributable to a federal disaster area.

Some additional tax credits and deductions have been adjusted for 2020 as follows:

- Child Tax Credit. The child tax credit has been expanded to $2,000 per qualifying child and is refundable up to $1,400, subject to phaseouts; there is a temporary $500 nonrefundable credit for other qualifying dependents.

- Earned Income Tax Credit (EITC). For 2020, the maximum EITC amount available is $6,660 for married taxpayers filing jointly who have three or more qualifying children (it’s $538 for married taxpayer with no children). Phaseouts apply.

- Adoption Credit. For 2020, the credit for an adoption of a child with special needs is $14,300, and the maximum credit allowed for other adoptions is the amount of qualified adoption expenses up to $14,300. The available adoption credit begins to phase out for taxpayers with modified adjusted gross income (MAGI) in excess of $214,520; it’s completely phased out at $254,520 or more.

- Student Loan Interest Deduction. For 2020, the maximum amount that you can deduct for interest paid on student loans remains $2,500. The deduction begins to phase out for single taxpayers with MAGI in excess of $70,000, or $140,000 for married taxpayers filing jointly, and is completely phased out for single taxpayers at $85,000 or more, or $170,000 or more for married taxpayers filing jointly.

- Lifetime Learning Credit. For the 2020 tax year, the adjusted gross income (AGI) amount for joint filers to determine the reduction in the Lifetime Learning Credit is $118,000; the AGI amount for single filers is $59,000.

- Medical Savings Accounts (MSA). For 2020, a high-deductible health plan (HDHP) is one that, for participants who have self-only coverage in an MSA, has an annual deductible that is not less than $2,350 but not more than $3,550; for self-only coverage, the maximum out-of-pocket expense amount is $4,750. For 2020, HDHP means, for participants with family coverage, an annual deductible that is not less than $4,750 but not more than $7,100; for family coverage, the maximum out-of-pocket expense limit is $8,650.

- Foreign Earned Income Exclusion. For tax year 2020, the foreign earned income exclusion is $107,600.

- Section 199A (Qualified Business Income). As part of the TCJA, sole proprietors and owners of pass-through businesses are eligible for a deduction of up to 20% for qualified business income. The deduction is subject to threshold and phased-in amounts. For 2020, the threshold amounts begin at $326,600 for married taxpayers filing jointly:

There is an additional standard deduction of $1,350 for taxpayers who are over age 65 or blind. The amount of the additional standard deduction increases to $1,700 for taxpayers who are unmarried.

There is an additional standard deduction of $1,350 for taxpayers who are over age 65 or blind. The amount of the additional standard deduction increases to $1,700 for taxpayers who are unmarried.